Cash flow quadrant 7 to 8 figures

Cash flow quadrant and 7, 8 figure mindsetIn this video I share the news that a new mindset and framework of optimized thinking...

CAsh flow quadrant step by step

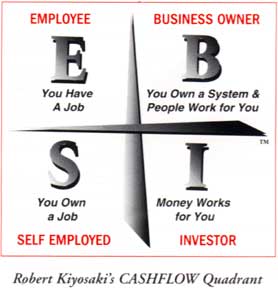

Full video click here: Cash flow quadrant notes…Investor Quadrant- Check out the article for rich dad cash flow quadrant here Time value of...

Cash flow quadrant transitioning

Solving the cash flow quadrant problem This video is about solving the cash flow quadrant problem of going from the 9-5 mindset to...

Cycles Cashflow and Minnesota Real Estate Investing

#Cycles, #cashflowquadrant and #mnrealestate In this video I discuss different cycles in life and how we move ourselves through the different cash flow...

How Minnesota Real Estate Investors Use Rich Dad Poor Dad Cashflow Quadrant ESBI by Robert Kiyosaki

How Minnesota Real Estate Investors Use Rich Dad Poor Dad Cashflow Quadrant ESBI by Robert Kiyosaki

How MN Real Estate Investors can learn Cashflow Quadrant by Robert Kiyosaki

How MN Real Estate Investors can learn Cashflow Quadrant by Robert Kiyosaki Minnesota Real Estate Investors Employee and Self-Employed When listening to Robert...

Worry when selling your MN house as-is fast

Worry when selling your MN house as-is fast

Disappointment when selling your MN house as-is fast

Disappointment when selling your MN house as-is fast

Overwhelmed when selling your MN house as-is fast

Overwhelmed when selling your MN house as-is fast

Frustration, Irritation, and Impatience when selling your MN house as-is fast

Frustration, Irritation, and Impatience when selling your MN house as-is fast

Pessimism when selling your MN house as-is fast

Pessimism when selling your MN house as-is fast

Boredom when selling your MN house as-is fast

Boredom when selling your MN house as-is fast

Contentment when selling your MN house as-is fast

Contentment when selling your MN house as-is fast

We buy houses investors sell my MN home as-is fast for cash

Cash offer on motivated Minnesota home sellers homes

How to Sell My MN House Cash or Seller Financing Offer | We Buy Houses

"Ron I'm ready, I've decided it's time, I must sell my house quickly As-Is for a fast cash offer!"

Is your Minnesota house and real estate in probate court, sell as-is fast cash

is your Minnesota house and real estate in probate court, sell as-is fast cash Talking to others that have helped motivated sellers...

Did renters recently trash your Minnesota house Sell as-is fast cash

Burnt out landlords…Did renters recently trash your Minnesota house Sell as-is fast cash It’s a nightmare scenario for a burnt out landlord....

Are you stuck with an inherited Minnesota house sell as-is fast cash offer

Are you stuck with an inherited Minnesota house sell as-is fast cash offer Your brother, sister and siblings are trying to get...

Are you making two Minnesota house payments?sell as-is fast cash

Are you making two Minnesota house payments? Sell as-is fast cash If you have two Minnesota house payments that you are making...

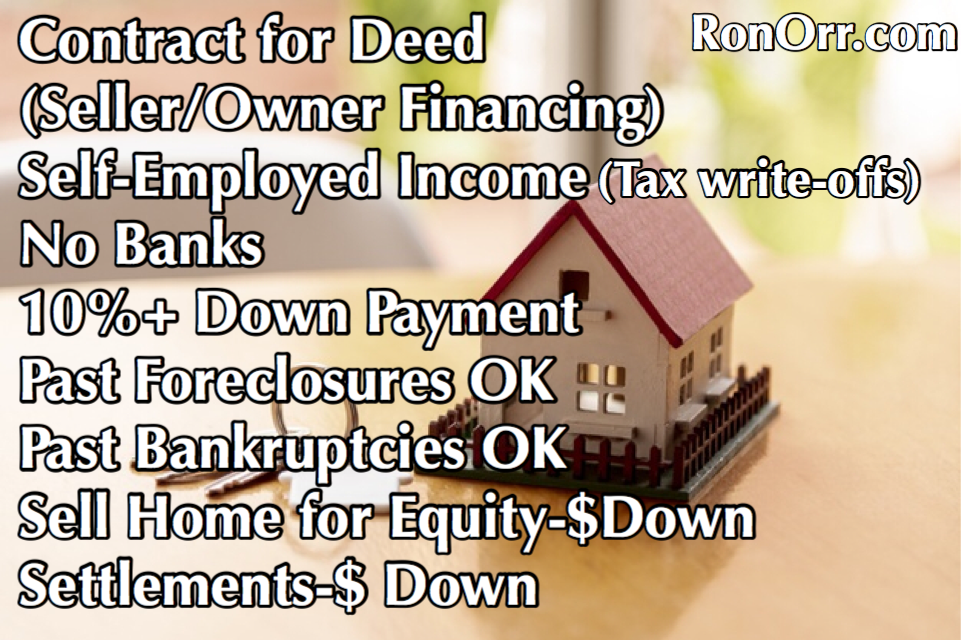

I’m forced to sell my Minnesota home as-is fast for equity to have a down payment to buy on a contract for deed

I’m Forced to sell my Minnesota home due to my bad credit sell as-is quickly Because you can not easily get financed...

Trapped equity? Sell your Minnesota home fast as-is

Trapped equity? Sell your Minnesota home fast as-is You have a house right here in Minnesota and it may even be vacant,...